Last night, news broke that pharma giant Eli Lilly was

in talks to acquire Verve Therapeutics. After

a 3-year lull in major CRISPR dealmaking following the Covid bubble, this brings

the space the Big Pharma validation that genome editing is not a crazy fantasy,

but a core modality of future drug innovation. To my surprise, even hardcore biotech

investors had been waiting for such validation before considering the space investable.

Last night, news broke that pharma giant Eli Lilly was

in talks to acquire Verve Therapeutics. After

a 3-year lull in major CRISPR dealmaking following the Covid bubble, this brings

the space the Big Pharma validation that genome editing is not a crazy fantasy,

but a core modality of future drug innovation. To my surprise, even hardcore biotech

investors had been waiting for such validation before considering the space investable. Needless to say, the news will trigger pin action in other CRISPR stocks. In this blog post, also based on a similar experience I had in the RNAi space about 10 years ago, I will lay out how I see it play out,

Verve acquisition is a steal

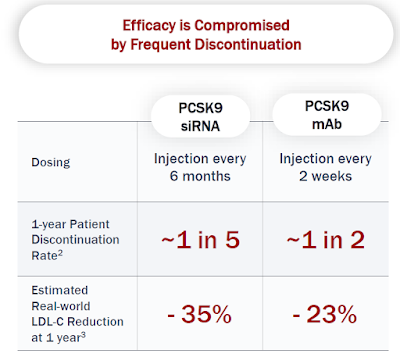

As you will remember, Verve is developing an exciting one-time PCSK9 base editing treatment, VERVE-102, that could transform LDL-cholesterol-driven

atherosclerotic cardiovascular disease (ASCVD).

According to the rumors in the Financial Times the

proposed acquisition price is ~$1.3B. This would be a bargain considering the potential of VERVE-102.

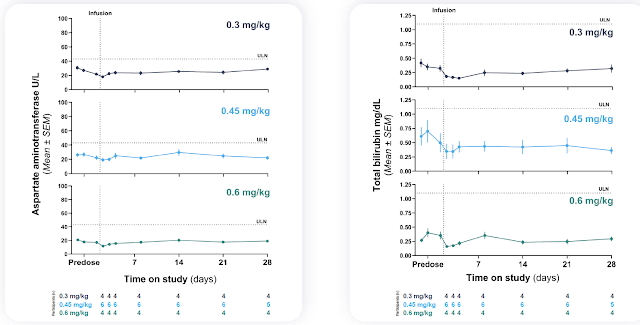

Even with the current small available safety dataset,

it is hard for me not to see VERVE-102 as a highly compelling option for the

1-2 million heterozygous familial hypercholesterolemia (heFH) population in the

US and Europe alone. Slap on that a $100,000

treatment price, this alone has Glp1-type market dimensions.

Under normal market conditions, such a steal would not be

possible. But these have been anything

but normal biotech investment times. I believe that more than the nice

short-term financial reward of an acquisition, Verve management is doing here

what is best for VERVE-102 reaching its maximal potential. Ultimately, it takes the financial resources,

experience, and credibility of a pharma giant to develop and commercialize such

a revolutionary treatment to such a big market.

Who is next?

But luckily for investors, Verve Therapeutics has not

been the only severely undervalued CRISPR company. When Alnylam started to gain tremendous

traction in 2012-3 after demonstrating that you can make RNAi gene silencing work in humans, still working as a consultant to companies and investors

back then, I noticed how funds started to dig into who could be the next Alnylam

to invest in.

So on the back of very strong recent clinical data in

the space (VERVE-102, NTLA-2001/2, BEAM-302) and now the Big Pharma validation,

I expect the same dynamic to unfold here.

Intellia Therapeutics

The first obvious company to benefit from fund inflow should be Intellia Therapeutics. Verve Therapeutics

will be acquired mostly for a therapeutic candidate that has shown promise in the clinic.

Intellia therefore with not just one, but three clinically validated market

opportunities (ATTR-CM, ATTR-PN, HAE) and a reasonably large market cap of around

$900M and good trading liquidity for funds to take needle-moving positions in,

will come first on the radar.

What is more, almost the entire market cap can be

accounted for by its cash position and the stock has come down from a high of around

$200 4 years ago to $9. The main

reservation by the investor community has been that patients will prefer a daily pill over a futuristic-sounding

lifetime treatment, if not cure. I guess

they were wrong. Not only is Eli Lilly’s

proposed acquisition a vote of confidence in CRISPR modality, but the KOLs in

the ATTR and HAE field are already fully on board.

Beam Therapeutics

Beam with a market cap about 2x of Intellia’s will

also come into investor focus.

While I do have a small position in that company, it is by far not as big as

the one I have in Intellia.

This is because I consider uncertainties around its

two lead candidates, for sickle cell disease (SCD) and alpha-1-antitrypsin disease

(AATD), to be higher than for Intellia’s opportunities. Their sickle cell disease base editing should be superior to that of already approved Casgevy by Crispr Therapeutics and

Vertex Pharmaceuticals.

But will that be enough for the ex vivo autologous

hematopoietic stem cell approach to gain quicker commercial traction than

Casgevy? With regard to BEAM-302 for

AATD, I am still waiting for more clarity on the liver safety of their

(non-GalNAc) LNP. It was the new safety

standard set by VERVE-102 (GalNAc-targeted and ‘Novartis ionizable lipid’) that

makes VERVE-102 a viable therapeutic in the first place.

Prime Medicine

Having just cured p47phox variant chronic granulomatousdisease (CGD) which could entail a valuable priority review voucher, Prime

Medicine is now focusing on the relatively large severe genetic liver disease

opportunities of Wilson’s Disease and AATD.

While not as clinically advanced as Beam Therapeutics,

Prime Medicine has the benefit of learning from the LNP safety of the Intellia, Beam, and Verve programs. I therefore

expect them to bring forward a lower-risk GalNAc-enabled LNP similar to Verve’s

when it enters the clinic next year.

From a platform point of view, prime editing is the

future of CRISPR medicine due to its versatility and exquisite on-target

specificity. Prime Medicine with a

dominant IP position in prime editing, a market cap of $200M, much of which in

cash, is therefore a prime candidate for a Big Biotech/Pharma looking to make

use of that technology for its in-house targets.

Metagenomi

Going nowhere in its clinical pipeline, but generating

new, especially smaller CRISPR editors that could have delivery and immunologic

advantages, is Metagenomi. Its lead

candidate is a CRISPR-enabled gene drop-in approach for hemophilia A (MGX-001)

which it hopes to bring into the clinic in 2026.

While I consider Metagenomi’s gene drop-in data to be

industry-leading, there are questions around its safety profile since it will

involve not only LNP, but also AAV for systemic delivery. So while MGX-001 could be the first ‘gene

therapy’ for hemophilia with sustained transgene expression, Metagenomi’s

valuation will unlikely get recognition for it until actual clinical data.

The main reason why Metagenomi is interesting here is

that it is not only trading 70% below cash ($55M market cap, $200M cash), but

that it has an important partnership with Ionis Pharmaceuticals which could

view CRISPR as an increasingly important mechanism to shore up its commercial

ambitions in ASO-led franchises such as ATTR, HAE, and cardiovascular disease.

If I were Ionis Pharmaceuticals, I would just buy Metagenomi

for $200M, retire preclinical MGX-001 for little cost and thus get rid of my future

milestone and royalty obligations. Of

course, Ionis may prefer Prime Medicine for its more versatile technology.

Buying a platform-only company in this biotech tape is certainly not for the faint of heart and large funds will shy away from Metagenomic at least initially due to its small size and illiquidity. I can see it, however, emerge as an attractive second-wave opportunity should interest in CRISPR stocks be sustained enough. As a backstop, you still have Ionis Pharmaceuticals having to make a decision on investing further into Metagenomi later this year.

You may ask yourself why I have not mentioned the

biggest CRISPR company by market cap, $3.6B CRISPR Therapeutics. This is because of initially overoptimistic

expectation for Casgevy sales and with their recent RNAi deal spreading

themselves out too thinly and losing their cutting edge so early in the game. I would also like to see them disclose the

liver safety before attributing value to their first generation Cas9 nuclease-based

cardiovascular CRISPR franchise.

Disclosure: Verve

Therapeutics became my largest portfolio position after they

disclosed VERVE-102 data two months ago.

While smaller than my positions in Huntington’s disease gene therapy

company uniQure and RNA editing company ProQR, Prime Medicine and Intellia

Therapeutics are not far behind and very meaningful positions with close to 10%

portfolio weightings.

This is not financial advice. It is intended for those interested in contemplating

the stock market repercussions of the rumored Verve Therapeutics

acquisition. Buying a stock is the

simple part, successfully trading it for profit much more difficult.